Using the Consumer Expenditure Survey (CES) data from the Bureau of Labor Statistics (BLS), NAHB Economics research shows that a home purchase triggers additional spending on appliances, furnishings, and remodeling. Such spending typically exceeds that of non-moving home owners and persists for two years after moving.

The NAHB analysis compares spending behavior among three groups of single-family detached home owners: buyers of new homes, buyers of existing homes and non-moving owners. During the first two years after closing on the house home buyers tend to spend on appliances, furnishings and property alterations considerably more compared to non-moving owners. However, home buyers tend to be larger households with children, and on average wealthier, with higher levels of education and concentrated in urban areas. Any of these factors could potentially explain higher spending on appliances, furnishings and remodeling by home buyers. Thus, the NAHB analysis controls for the impact of household characteristics on expenditures, and, nevertheless, finds that a home purchase alters the spending behavior of homeowners and that otherwise similar homeowners spend more across all three categories compared to non-moving owners during the first two years after moving.

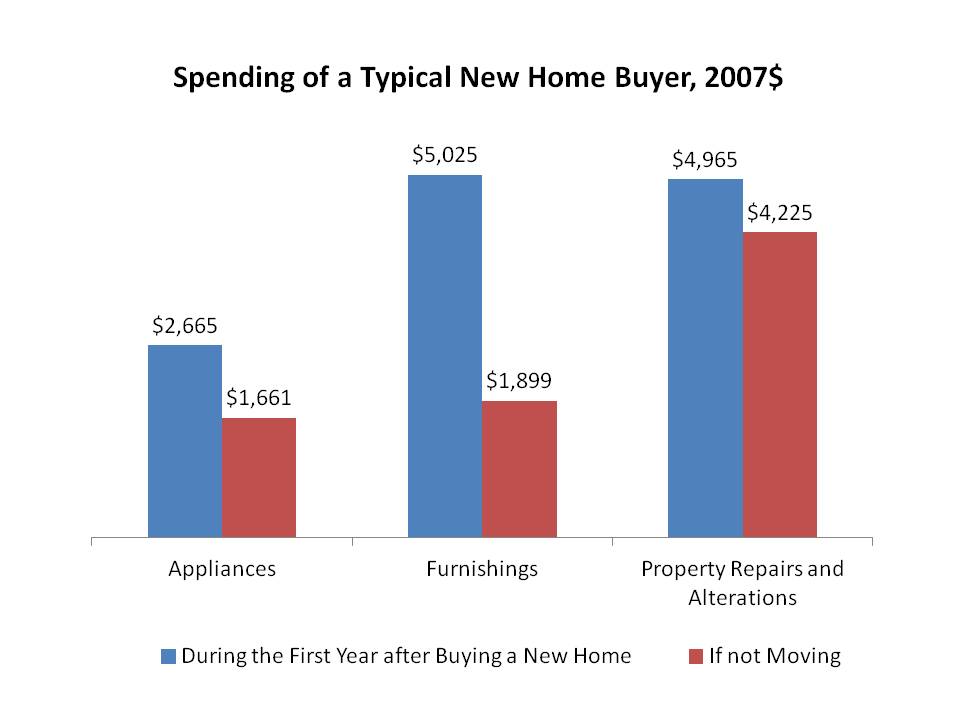

Looking at spending patterns of new home buyers and identical households that do not move, the differences are largest on furnishings. A typical new home buyer that buys a new home is estimated to spend in excess of $3,000 more on furnishings than an identical household that stays put in a house they already own. The elevated level of spending persists into the second year as new home buyers spend additional $2,000 over their typical budget on furnishings.

Similarly, moving into a new home triggers higher levels of spending on appliances. A typical new home buyer that moves into a new home is estimated to spend $1,005 more on appliances during the first year compared to a non-moving owner. The difference shrinks to $348 during the second year and goes away after that.

In the case of property repairs and alterations the differences are smallest, $740, and last only one year, which is not surprising considering that most households would not want to spend years in a house with ongoing remodeling projects.

Buying an older home also triggers additional spending. The typical buyer of an existing home tends to spend close to $4,000 more on remodeling, furnishings, and appliances compared to otherwise identical homeowners that do not move. However, in case of buying an older home, most of this extra spending goes to remodeling projects, more than $2,000, and occurs during the first year after closing on the house. Only the additional spending on furnishings tends to persist beyond the first year.

The statistical analysis further shows that this higher level of spending on furnishings, appliances and property alterations is not paid by cutting spending on other items, such as entertainment, transportations, travel, food at home, restaurants meals, etc. This confirms that home buying indeed generates a wave of additional spending and activity not accounted for in the purchase price of the home alone.

In summary, the NAHB analysis shows that during the first two years after closing on the house a typical buyer of a new single-family detached home tends to spend on average $7,400 more than a similar home owner who does not move, including $4,900 in the first year after purchase. Likewise, a buyer of an existing single-family detached home tends to spend about $4,000 more than a similar non-moving home owner, including $3,600 during the first year. The overall ripple effect of home buying does not stop here, as producers of appliances, furnishings and remodelers spend their additional income paid by home buyers and trigger further waves of economic activity.

Posted by Joshua J. Miller

Posted by Joshua J. Miller