Last week saw the release of yet another discussion draft from the staff of the Senate Finance Committee concerning tax reform. Following draft proposals concerning depreciation/accounting and other business expenses (such as advertising), the most recent draft proposes changes to the tax code’s rules concerning energy production and energy-efficient improvements.

Under the draft proposal, most existing energy tax incentives would be eliminated or otherwise allowed to sunset and replaced by two credits.

The first would be a tax credit for the production of clean energy, with the value of the credit determined by the amount of greenhouse gases produced during production – greener production, more credit. The credit could be claimed either as an energy production credit or an investment credit of up to 20% based on installed qualified equipment. The credit would become effective for new power production facilities after January 1, 2017, although after 2016 a 20% credit would be available for existing facilities that retrofit to capture at least 50% of carbon dioxide emissions. The credit would phase out when U.S. electricity production emits 25% less in greenhouse emissions.

The second credit would reward the production of any transportation fuel that is 25% cleaner than conventional gasoline. The maximum credit would be $1 per gallon, with the actual credit determined for the fuel relative to gasoline. The credit would begin in 2017. Alternatively, an investment credit would be available based on 20% of the value new, qualified production facilities.

In turn, the draft proposal would eliminate or phase out almost all existing energy tax incentives. For housing, this means:

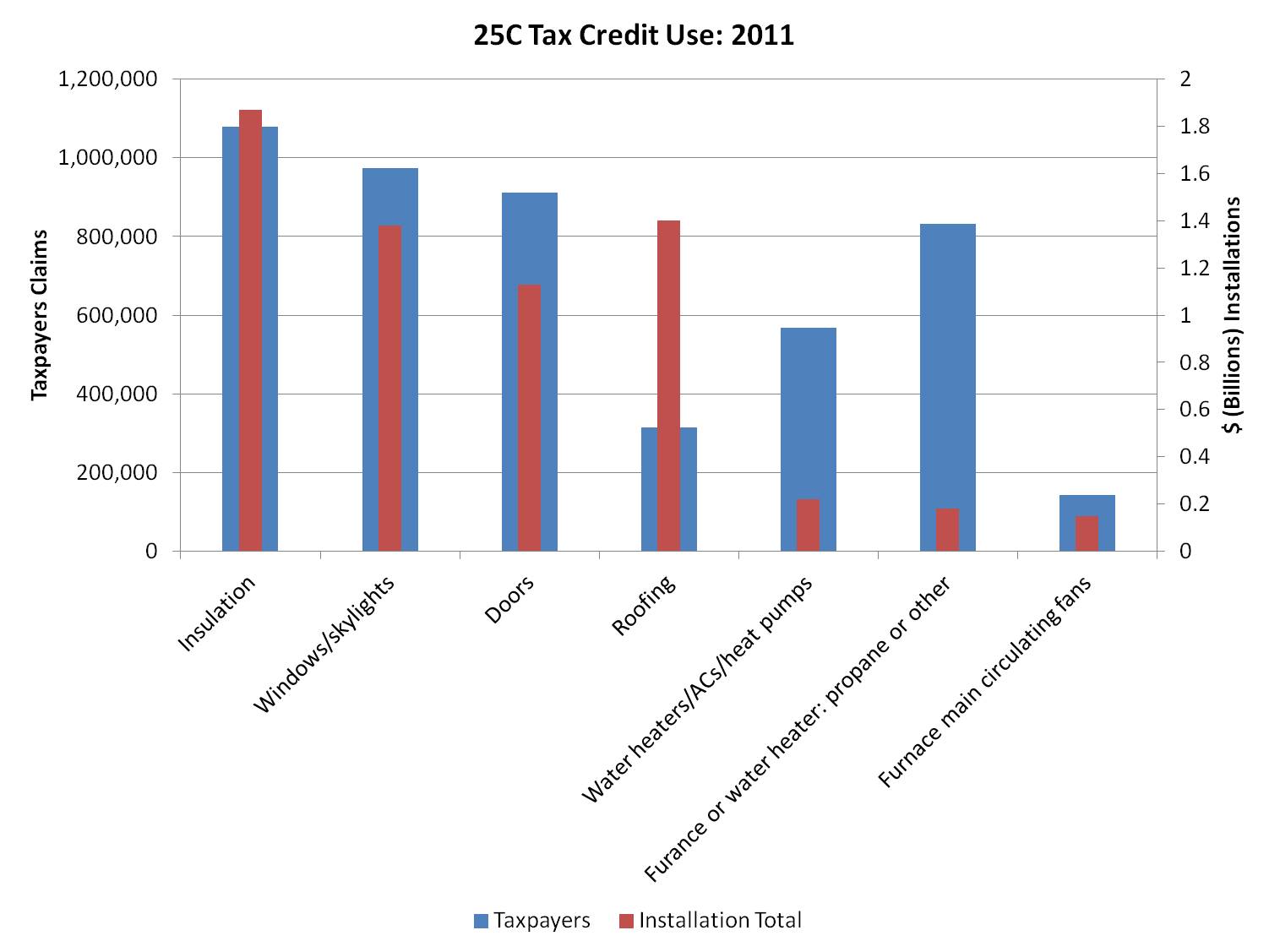

- The section 25C tax credit for energy-efficient improvements to existing homes would sunset permanently at the end of 2013

- The section 45L $2000 tax credit for the construction of new energy-efficient homes would sunset permanently at the end of 2013

- The section 179D credit for commercial and multifamily energy-efficient improvements, as proposed in the cost recovery draft, would be eliminated

The section 25D 30% tax credit for residential solar, geothermal, wind turbines, and fuel cells would remain under present law, but the December 31, 2016 sunset would be enforced.

It is estimated that these changes on net could raise $75 billion in tax revenue over ten years.

A number of general principles are embodied in this proposal, with negative consequences for housing and real estate measured against present policy.

First, the proposed approach would clearly favor energy production over energy conservation and retrofitting. Improving existing buildings, or constructing energy-efficient properties with long-run benefits for potential future owners, is an approach that is rewarded under the existing tax credit system.

Second, the proposed tax benefits for energy production appear to exclude homeowners and perhaps some rental housing and commercial real estate owners. The proposed legislative drafts indicate that for a taxpayer to qualify for the investment credit (as homeowners can do now under the 25D credit), the installed property must be eligible for depreciation. Homeowners do not claim depreciation deductions, so it appears power produced by an owner-occupied home would not be eligible. Furthermore, to qualify for the first tax credit noted above, any electricity produced on site must be sold to either an unrelated party or metered and monitored by a third-party. This rule may exclude some apartment and commercial real estate owners from the proposed tax rule for on site power production.

If this preliminary analysis is correct, excluding on-site power production is a policy mistake given such production does not suffer from transmission losses. According to the Department of Energy’s Energy Information Administration (EIA), “annual electricity transmission and distribution losses average about 7% of the electricity that is transmitted in the United States.”

NAHB will continue to review the proposal, which could be included in future comprehensive tax reform proposals, and submit comments to the Senate Finance Committee in January. In meantime, discussion is beginning to pick up concerning energy tax extender items, including the section 25C and 45L credits, which expire at the end of 2013.

Posted by Robert Dietz

Posted by Robert Dietz